The following methodology applies to this publication – Student loans forecasts for England, financial year 2025-26 only. Methodologies relating to previous publications can be found at this link Archive Timeline - UK Government Web Archive (opens in new tab).

Income Contingent Repayment (ICR) student loans are provided by Government to higher education students and some further education students to cover course fees and living costs while they are studying. They were first introduced in the UK for new undergraduate students in 1998, at the same time as tuition fees. Prior to 1998, university students were provided funding by Government through a mixture of grants and, from 1990, mortgage-style loans that were available to help with living costs. Mortgage-style loans are not covered in this publication.

Each of the four constituent countries of the UK now have their own student loan policies, but only students who are eligible through Student Finance England (SFE) are considered in this publication. These are loans issued to English-domiciled students at UK providers and a small number of students of other residencies that attend learning providers in England. A summary timeline of income-contingent repayment loans is available in Table 1.1 below.

Table 1.1: Income Contingent Repayment loan timeline: England

1998

Plan 1 loans introduced for new UK domiciled undergraduate students, to cover living costs.

Annual tuition fee of up to £1,000 also introduced in 1998 Teaching and Higher Education Act.

2006

Maximum annual tuition fee limit increased to £3,000 for new full-time undergraduate entrants.

Tuition fee loans introduced to meet the costs of tuition for new full-time undergraduates.

Maintenance grants introduced for new full-time undergraduate entrants on lower incomes.

EU domiciled students became eligible to take out tuition fee loans.

Repayment term changed to 25 years for new entrants, rather than ending at age 65.

2012

Plan 2 loans introduced for new entrants.

Maximum annual tuition fee limit increased to £9,000 for new full-time undergraduate entrants.

New eligible part-time undergraduates subject to maximum tuition fee limit of £6,750 and entitled to fee loans for the first time to meet the full costs of their tuition.

2013

Advanced Learner Loans introduced for students aged 24+ on designated Level 3-4 further education courses in England, on the Plan 2 system. Advanced Learner Loans Bursary Fund introduced.

2016

Plan 3 loans introduced for new students taking postgraduate Master’s courses, who could borrow up to £10,000 over the length of their course.

Maintenance grants replaced by additional loans for living costs for new full-time undergraduate entrants on lower incomes.

Advanced Learner Loans and Bursary Fund extended to students aged 19-23 and to Level 5-6 designated courses.

2017

Nursing, midwifery and most allied health students become eligible for student loans, in place of receiving NHS bursaries.

Maximum annual tuition fee limits increased for new entrants and continuing students who started their courses on or after 1 September 2012 (£9,250 for a full-time course, £6,935 for a part-time course).

2018

Plan 2 repayment threshold increased from £21,000 to £25,000. It had previously been announced that it would remain at £21,000 until April 2021.

Doctoral degree loans of up to £25,000 across the length of a borrower’s course introduced for new starters, on the Plan 3 system.

Loans for living costs introduced for new part-time undergraduates attending degree-level courses and level 5 pre-registration healthcare courses only.

2019

Plan 2 repayment threshold increased to £25,725 for tax year 2019-20, and was thereafter increased annually in-line with average earnings growth figures published by the Office for National Statistics (ONS) until subsequent freezes were announced.

2020

Plan 3 repayment threshold remains at £21,000 until April 2022.

2021

Student Finance support for EU Domiciles withdrawn.

2022

Plan 3 repayment threshold remains at £21,000 until April 2023

Plan 2 repayment threshold remains at the financial year 2021-22 level of £27,295 until April 2025 increasing annually with RPI (Retail Price Index) rather than earnings thereafter

Interest rate for plans 2 and 3 capped at 7.3% for academic year 2022/23 in line with forecast prevailing market rate

2023

Plan 3 repayment threshold remains at £21,000 until April 2024

Plan 5 loans introduced for new entrants starting from 1st August 2023, with repayment threshold at £25,000 until April 2027 (increasing annually with RPI thereafter), a repayment term of 40 years and a rate of interest in and after study of RPI+0%

Maximum annual tuition fee limits frozen at 2022/23 levels for the 2023/24 and 2024/25 academic years for new and continuing undergraduate students (£9,250 for full-time courses, £6,935 for part-time courses)

2025

Plan 3 repayment threshold remains at £21,000 until April 2026

Plan 2 repayment threshold freeze ended in April 2025. Threshold increased to £28,470 reflecting RPI outturns.

Maximum annual tuition fee limits increased for new and continuing undergraduate borrowers in the 2025/26 academic year to £9,535 for full-time courses and £7,145 for part-time courses at providers with a TEF award.

2026

Plan 2 repayment threshold to be frozen at 2026-27 levels until April 2030, when it will return to increasing with RPI, as announced at the 2025 Autumn Budget.

Plan 3 repayment threshold remains at £21,000 until April 2027.

Plan 2 and Plan 3 interest rates capped at 6% for the 2026/27 academic year.

Student loans are issued and administered by the Student Loans Company (SLC) on behalf of the Government and the devolved administrations in the UK. The Department for Education produces forecasts for its outlay on, and the repayments it expects to receive from, the English student loans that it is responsible for. These forecasts are audited by the National Audit Office (NAO) annually and are subject to the Department for Education’s quality assurance framework for business-critical models. The forecasts are scrutinised and cleared by quarterly internal Models and Funding Boards before they are used in financial planning, policy development and to value the loans that have been issued in its annual accounts. The forecasts presented in this publication are produced across multiple models, as follows:

Entrant borrowers model – this model forecasts the annual growth in the number of full-time undergraduate loan borrowers in year one of their course, studying at providers eligible to charge for the maximum annual tuition fee loan amount. This makes up the majority of the full-time undergraduate loan borrowing population. The growth rates from this forecast are applied to the latest year of outturn SLC data (academic year 2024/25) in the student loan outlay model.

Student loan outlay model – this model produces forecasts of loan outlay on higher education ICR loans issued to undergraduate and postgraduate students.

Student loan earnings model – this model produces forecasts for the future earnings of higher education ICR loan borrowers.

Student loan repayments models – separate undergraduate and postgraduate models produce forecasts for the future repayments that will be made by higher education ICR loan borrowers.

Advanced Learner Loans model – this model produces forecasts for loan outlay and repayments that will be made on Advanced Learner Loans, which are available for some further education courses.

This document provides information on these models, including the methodology, data sources and assumptions used in producing the forecasts.

With the exception of the Lifelong Learning Entitlement (LLE) (opens in new tab), these forecasts incorporate existing government policy announced by April 2026, which is when this forecast was approved by DfE. From September 2026, learners will be able to apply for LLE funding for courses and modules commencing from January 2027 onwards. The introduction of the LLE, and any other changes to student loan eligibility, loan amounts, or terms and conditions, if implemented by Government after 27 April 2026, are not accounted for in the forecasts in this publication. The policy to cap interest rates at 6% in academic year 2026/27 for Plan 2 and Plan 3 loans is included in these forecasts.

DfE’s higher education (HE) undergraduate (UG) entrant borrower model forecasts the annual growth in full-time undergraduate Student Finance England loan borrowers commencing a new course. The growth rates from this forecast are applied to the latest year of outturn SLC data (academic year 2024/25) in the student loan outlay model, which informs the department’s financial accounts of Student Finance England student loan outlay.

Courses eligible for public funding via student loans may be delivered by a lead provider or by a partner institution (franchised provider) on behalf of the lead provider. Lead providers are the higher education institutions students register with; they retain overall responsibility for a course delivered, including responsibility for its quality, standards, and oversight, even when that course is delivered under a subcontractual (franchised) arrangement. Franchised providers are the partner organisations that run courses on behalf of lead providers under subcontractual arrangements. At present, lead providers must register with the Office for Students so that their students can access student loans, but franchised providers need not.

Growth in franchised provision has accelerated in recent years. In response, the Department launched a sector-wide engagement programme in 2025 to address concerns of fraud, abuse of public money and poor value for students. To capture this growth accurately and estimate how the Department’s engagement will affect it, the entrant borrower model forecasts the growth in franchised and direct provision separately.

Scope

The UG entrant borrowers forecast covers student entrants who are entitled to both tuition fee and maintenance loans, have taken out a SFE student loan and are studying a level 4, 5 or 6 course. These students are registered with an Approved (fee cap) (opens in new tab)providers in England or a Higher Education provider in Scotland, Wales and Northern Ireland; Approved (fee cap) providers are eligible to charge the maximum annual tuition fee loan amount (£9,790 in academic year 2026/27).

The following borrowers are excluded from the entrant borrowers forecast:

Borrowers whose loans are administered by the Devolved Administrations.

Borrowers who are not eligible to take out a maintenance loan according to the regulations (referred to as partial support).

Borrowers studying at Approved providers in England (or being charged the Approved fee amount).

Borrowers who are not in the first year of their course (referred to as returning students).

Undergraduate SFE loan borrowers that fall in group 3-5 are captured separately within DfE’s higher education student loans outlay model.

The UG entrant borrower model does not cover any entrants that have not taken out a Student Finance England student loan. The population in scope includes a small number of EU nationals with pre-settled residency status who are entitled to Student Finance England loans as a result of the UK–EU Withdrawal Agreement. This small group of entrant borrowers are forecast separately from the rest of the undergraduate borrower population because their numbers will decrease substantially in 2026, once the EU pre-settled status ceases to exist.

SLC administrative data inclusive 2024/25, as of 31 August 2025.

Entrant borrowers

The historical number of entrant borrowers in each academic year is derived from administrative data obtained from the Student Loans Company. A borrower is counted if they are on the first year of a new course, has taken out a loan from SFE (fee and/or maintenance) and fits the scope of the target population (see “Scope” section above). Borrowers are aggregated by academic year (2013/14-2024/25), sex (male, female), age group (18 and under, 19, 20, 21-24, 25-34 and 35 and over), and provision type (direct provision or franchised provision). Direct provision entrants are entrants whose course is run by the lead provider, while franchised provision entrants are entrants whose course is run by a subcontracted provider that delivers the course on the lead provider’s behalf (see Franchising adjustment forecast, below for more detail).

Direct provision borrower counts are divided by the number of people in the general population to obtain the proportion of the population that has taken out a loan in each age-sex subgroup - we refer to this proportion as the borrower rate. Franchised provision counts are modelled without conversion into borrower rates to reduce volatility in the fitted timeseries. The latest data from the Student Loans Company has an effective date of 31 August 2025 and contains borrowers for academic years up to and including 2024/25.

Population

It is assumed that ONS population data for England are a suitable proxy for the underlying population of the Student Finance England borrower population. ONS population estimates and projections are aggregated by sex (male, female) and age group (18, 19, 20, 21-24, 25-34 and 35-60). These estimates and projections are used as the denominator population count for each age-sex group of borrowers to obtain the borrower rate. Population counts for 18-year-olds are used as the denominator for borrowers aged 18 and under, and population counts for people aged 35-60 are used for borrowers aged 35 and over, as borrower numbers for people aged under 18 and over 60 are very small.

Main scheme applicants

Main scheme applicants refer to applicants who apply through the UCAS application system by the end of June (exact date varies from year to year). January deadline applicants are a subgroup of main scheme applicants who apply by the interim deadline, in January (date also varies annually). January deadline applicants make up the majority of main scheme applicants, but not all of them. The entrant borrowers model uses the January deadline figures to predict the number of borrowers in the second forecast year (2026/27), because at the time of the model update included in this publication, only the January deadline data had been published. These numbers do not include applicants who applied for the first time through UCAS clearing or applicants who made applications directly to providers.

The entrant borrower model uses these lead indicator applicant figures to predict the number of direct provision borrowers expected in the second forecast year, using the historical trend in the annual ratio between applicants and borrowers. In the current version of the forecast, this data was used for estimating the borrower numbers of entrants aged 20 or under in the second year of the forecast.

Main scheme accepted applicants

The entrants model uses UCAS end of cycle acceptances data that cover the number of applicants that were accepted through UCAS main scheme or UCAS clearing application systems. It uses these lead indicator figures to predict the number of borrowers in the first year of the forecast in direct provision groups.

Sex and gender classifications

The Student Loans Company records borrower’s sex and provides two options (male and female). UCAS data reports applicant’s gender and provides several options. While these two classifications do not completely align, using gender from the applicant and accepted applicant data as a proxy for sex in the borrower data will have minimal impact on the overall accuracy of the forecast and is deemed valid for the current purpose. Instances where the gender is not ‘woman’ or ‘man’ in UCAS data are combined with female applicants or accepted applicants because females account for the largest number of entrants. This assumption has made minimal impact to the forecast historically and is continually being reviewed.

Methodology

The entrant borrowers model forecasts annual growth in entrant borrowers over a six-year period. Forecasts are run separately for each age group, sex and provision type group, or stratum. Before they are modelled, direct provision figures are converted to borrower rates. Franchised provision counts are modelled without conversion.

Model structures

Each direct provision stratum is forecast using either a one-stage or a two-stage model structure. A one-stage structure projects the historical trend in borrower rates or borrower counts from SLC data forward in time to the end of the forecast period. A two-stage structure first predicts the number of borrowers in the first 1 to 2 years of the forecast using the historical trend in the ratio between borrower numbers and UCAS lead indicator figures. These predictions are appended to the historical timeseries of borrower data, and the combined trend is fitted and projected forwards over the remaining 4-5 years of the forecast in stage two, depending on whether one or both of the lead indicator data sources were used.. These lead-indicator models capture the predictive power of the UCAS data, including the uncertainty in how UCAS figures have historically translated entrant borrower numbers in SLC data. The model does not assume that a single model structure will perform well across all age/sex/provision-type strata, so initially all strata are fitted with both structures.

Franchised provision strata are forecast using only a one-stage model to obtain a forecast that reflects the potential growth that would have occurred had the Department not taken engagement action in 2025. The impacts of the enforcement action on future entrant numbers are modelled separately and the reduction of entrants expected is applied in the outlay model.

Forecasting approaches

The model also does not assume that a single fitting approach will perform well across all strata either, so each structure (in all strata) is also fitted with a range of fitting approaches. Both the two-stage and trend-only forecasts are run using exponential smoothing (ETS) models and random walk models, with and without a drift term.

The lead indicator models, run in the first stage of the two-stage model, are fitted with an ETS model and a random walk model without drift. The latter is used when there is a high level of uncertainty regarding the direction of the trend, or the back series is noisy.

Exponential smoothing (ETS) models

ETS models forecast future borrower rates or counts by applying weighted averages to past observations, giving greater emphasis to recent data so that new data influences the forecast more strongly than older ones. This approach allows the model to adapt quickly to changes while still considering historical patterns. ETS models can dampen trends, meaning they gradually flatten the slope of the forecast over time to avoid unrealistic long-term growth or decline. They can also control how responsive the forecast is to new data when setting the trend component, and how quickly the forecast updates its estimate of the current level based on new observations. These are varied using Phi (φ), beta (β) and alpha (α) parameters, respectively. A model with low values of α and β reacts slowly, favouring stability, whereas high values favour reactivity. Lower values of φ produce stronger damping, whereas higher values allow the trend to persist for longer.

For an ETS model with additive trend and dampening:

Data is fitted with ETS variants, with different β (beta) values, designed to vary how quickly the trend responds to new data:

Short-term (β = 0.7) highly responsive

Medium-term (β = 0.4): moderately responsive

Long-term (β = 0.1): less responsive

In all three ETS variants, alpha (α) is fixed at 0.7, ensuring that the level component remains stable and avoids introducing artificial growth or decline in the first year that is forecast. This choice reflects the aim for a smooth, realistic transition from historical data or lead indicator prediction to forecast. Phi (φ) is fixed at 0.9, which represents a modest amount of dampening. Together, these settings allow us to balance responsiveness and stability across different forecasting horizons and preserve the ability to explain the drivers of the forecasts.

The lead indicator models used to predict borrower numbers from UCAS figures in the first one to two years of the forecast are fit with an ETS model that responds quicky to new data when setting the level (alpha 0.7), reacts moderately when setting the trend (beta 0.5) and applies minimal dampening (phi 0.95).

Model selection

The best forecast for each stratum is chosen based on its performance in back testing relative to the other candidate models, analytical judgement and policy intelligence. Thus, the forecasts of some strata may be informed by UCAS lead indicator data because that data has predictive power - while others may be driven only by historical trends in borrower rates, because the lead indicator data performs worse or more noisily than the historical trend alone and risks producing a less accurate forecast. Likewise, some forecasts may have been produced with a long-term ETS model because it is assumed that recent growth is equally informative of the future as growth observed in earlier years, while others may be fitted with a medium-term ETS model - which puts less weight on the earliest years than the long-term model - because those earlier years are deemed to be less representative of future growth, for example due the trend changing. A random walk model is chosen when there is no obvious trend in the historical data or a high level of uncertainty regarding direction of growth.

The models chosen for the direct provision section of the forecast in this publication are shown in Table 2.1. All franchise provision strata are fitted with a medium term ETS, one-stage model.

Table 2.1: Models chosen for the direct provision section of the forecast

Stratum

Forecast Year 1

Stratum

Forecast year 2

Stratum

Approach taken to fit

Age 18 and under, Females

Predicts borrowers using the historical ratio between borrowers and total accepted applicants

Age 18 and under, Females

Predicts borrowers using the historical ratio between borrowers and main scheme applicants who applied by the January deadline.

Age 18 and under, Females

ETS long term

Age 18 and under, Male

Age 18 and under, Male

Age 18 and under, Male

Age 19, Females

Age 19, Females

Age 19, Females

Age 19, Males

Age 19, Males

Age 19, Males

Age 20, Females

Predicts borrowers based on the projected ratio between borrowers and accepted applicants (main scheme and direct-to-clearing routes only) using ETS lead indicator model.

Age 20, Females

Age 20, Females

Age 20, Male

Age 20, Male

Age 20, Male

ETS medium term

Age 21-24, Female

Age 21-24, Female

No lead indicator, as UCAS main scheme applicant data is not predictive of borrower numbers in these strata.

Age 21-24, Female

ETS long term

Age 21-24, Male

Age 21-24, Male

Age 21-24, Male

Age 25-34-Female

Age 25-34-Female

Age 25-34-Female

ETS medium term

Age 25-34-Male

Predicts borrowers using the historical ratio between borrowers and accepted applicants (main scheme and direct-to-clearing routes only) using random walk lead-indicator model.

Age 25-34-Male

Age 25-34-Male

Age 35 and over, Females

Predicts borrowers using the historical ratio between borrowers and accepted applicants (main scheme and direct-to-clearing routes only), projected with an ETS lead indicator model.

Age 35 and over, Females

Age 35 and over, Females

Random walk

Office for Students (OfS) registration

Since academic year 2019/20, providers in England (offering higher education courses) that wish to charge the maximum tuition fee amount are required to register with the OfS under the Approved (fee cap) (opens in new tab) category (opens in new tab). The entrant borrowers forecast captures the growth in entrants at lead providers that registered as Approved (fee cap) by 31st August 2025. The forecast does not include entrants at providers that are yet to register as Approved (fee cap). The entrant borrowers model does not include the students at Approved providers; these loan borrowers are captured within DfE’s higher education student loans outlay model.

NHS Long-term Workforce Plan

The NHS Long-term Workforce plan (opens in new tab) aims to significantly expand the number of training places for healthcare courses over the next decade, including medicine and dentistry, nursing, midwifery and subjects allied to medicine, with a particular focus on areas facing staff shortages. The impact of these additional training places on the number of borrowers expected over the forecast period was estimated together with the Department of Health and Social Care (DHSC) and is included in this forecast.

Franchising adjustment forecast

The Department has undertaken a programme of sectoral engagement to address the risk about fraud, abuse of public money and poor value for students caused by the rapid growth of franchised provision where this is not supported by sufficiently robust oversight and controls.

The behavioural response impact of this engagement action on future entrant numbers was estimated using a two-part microsimulation model. In the first stage of the model, franchise arrangements are allocated to one of four strategies (continued growth, maintaining their current cohort size, shrinking over time, or ceasing recruitment altogether). In the second stage of the model, the impacts of these strategy choices are then applied to future entrants, who may remain in franchised provision, be displaced into non-franchised HE provision or may choose not to enter HE.

The number of students in each academic year estimated to no longer enter HE due to reduced capacity at franchised providers forms the ‘franchising adjustment’ forecast. This franchising adjustment forecast is used in the outlay model to adjust the future borrower population, removing the appropriate number of entrants from future franchised provision.

This forecast does not yet include impacts of the Department’s requirement for most franchised providers with more than 300 students to register with the Office for Students.

Forecast

Table 2.2 shows the forecast for full-time undergraduate entrant loan borrowers at Approved (fee cap) providers in England and providers in the Devolved Administrations eligible to charge the maximum loan amount, before and after policy amendments are applied.

Table 2.2: Forecast for full-time undergraduate entrant loan borrowers at Approved (fee cap) providers in England and Higher Education providers in the Devolved Administrations

Academic Year

Direct provision (before additions)

Franchised provision (before removals)

Total forecast before policy additions and removals

Total forecast incl. additions and removals

Annual growth rate, total forecast incl. additions and removals

2025/26

364,800

70,000

434,800

429,900

1.9%

2026/27

372,700

75,400

448,100

441,700

2.7%

2027/28

373,200

80,700

453,900

445,800

0.9%

2028/29

374,000

85,800

459,800

451,900

1.4%

2029/30

376,900

90,900

467,800

459,800

1.7%

2030/31

378,400

95,900

474,300

465,500

1.2%

Long-term forecasts

Beyond the six-year forecasting period, growth in loan-eligible entrants is forecast using ONS population projections, weighted according to the age make-up of the borrower population. This forecast is used in the student loans outlay and the student loans repayment models. Separate projections are produced for full-time and part-time undergraduate entrants, and for Master’s and Doctoral entrants. To obtain these growth rates, ONS principal population projections for each age are first converted into cumulative growth rates, with the final year of the short-term forecast as the baseline (i.e. academic year 2030/31). For undergraduates, these are then weighted according to the distribution of age observed in the last forecast-year of the Student Loans Outlay Model with the effective date of November 2024. Student Loans Outlay Model sampling (which the forecast is dependent on) identifies age at course start date of the loan-borrowing entrant from the difference in years between the date of birth and the course start date. For Master’s and Doctoral entrants, the growth rates are weighted by the age distribution of borrowers in SLC data for academic year 2019-2021. At the time of this analysis, the effective date of the SLC data was April 2023. For each study level, weighted growth rates are then summed across age to obtain total cumulative growth (i.e. for each of the student population), from which the year-on-year growth is then calculated.

Data quality

The nature of any forecast is inherently uncertain and dependent on the quality of the source data, modelling methodology and model assumptions. The entrant borrowers model uses published data from ONS and UCAS as well as administrative data from the Student Loans Company to forecast full-time undergraduate entrants.

ONS Population Estimates and Projections

ONS population estimates and projections used in the short‑term and long‑term entrant borrower models are fully accredited official statistics and the primary population statistics used across Government. ONS figures are produced as mid‑calendar‑year estimates, whereas entrant borrower forecasts are run on an academic‑year basis (generally September to August). While this misalignment may have a small impact on forecast accuracy, ONS population projections are considered sufficiently robust for modelling purposes, as most full‑time undergraduate entrants commence study in the first calendar year of the academic year, which broadly aligns with the population data.

Data quality guidance for population projections (opens in new tab) and estimates (opens in new tab) is published by ONS. Short-term principal projections are largely considered reliable; given that the entrant borrowers model only forecasts over a six-year period, this increases confidence in the base population which forecast entrant are modelled from. ONS do not make any predictions of future political or economic changes that could affect population numbers.

UCAS data

The model uses open access statistical reports published by UCAS on higher education applications and acceptances at various points in the cycle. UCAS voluntarily apply (opens in new tab) the Code of Practice for Statistics to their statistical releases and their releases are considered reliable.

Limited historical coverage following the £9,000 tuition fee reform

The entrant borrowers model relies on a relatively short and recent historical series, which increases forecast uncertainty and sensitivity to unusual movements in the data. This is because data prior to funding reforms in academic year 2012/13 are not representative of future borrower behaviour, given the substantial changes to tuition fee levels and student finance arrangements following the increase to £9,000 per year. The use of post‑reform data only improves relevance but reduces the number of usable observations, making the model more exposed to short‑term fluctuations, including those driven by policy changes and the Covid‑19 pandemic.

Impact of international students on the entrant loan borrowing population

No assumptions are explicitly made regarding the growth of international students and what impact it might have on the growth of the SFE loan-borrowing entrant population. Given the many factors that influence international applicant demand, there are limited sources of forecasts. However, we continue to monitor UCAS and HESA data. Recent policy changes mean future growth is uncertain; however, this is assumed to have little effect on the growth of domestic student entrants because international students account for a relatively small proportion of the full-time undergraduate student entrant population.

Entrant borrowers model uncertainties

There is uncertainty around provider capacity, including whether providers will be able to continue growing at the current rates and how long they will be able to continue growing for. Provider behaviour during the 2025/26 UCAS acceptance cycle suggests that at least some providers, such as those UCAS refers to as “high tariff” providers are trying to grow by making more acceptances than in previous years and accepting applicants earlier in the cycle than in previous years.

The postgraduate entrant borrowers model forecasts the number of postgraduate students expected to take out a Student Finance England postgraduate loan for a Master’s or Doctoral degree, over a six-year forecast period. The forecast borrower numbers are used in the Outlay model which informs the department’s financial accounts of Student Finance England student loan outlay.

Scope

The forecast covers entrant loan borrowers that have taken out a Student Finance England postgraduate loan and are registered at an HEI providers in England and the Devolved Administrations. These are students that are eligible for student loans because they have been ordinarily domiciled in England for at least 3 years before the start of their course. The population in scope includes a small number of EU nationals with pre-settled residency status who are entitled to Student Finance England loans as a result of the UK–EU Withdrawal Agreement. This small group of entrant borrowers are forecast separately from the rest of the postgraduate borrower population because their numbers will decrease substantially in 2026, once the EU pre-settled status ceases to exist.

Data

The data used for the forecast is provided by SLC throughout the year and contains aggregate numbers of postgraduate Student Finance England entrant borrowers taking out loans for Masters and Doctoral courses, for each academic year. The most recent data set has effective date of 31 January 2026 and includes academic years up to and including 2025/26. The SLC payment cycle can run for a year longer than the academic year does, as borrowers can apply up to 9 months after the day their course starts and courses can start at various points throughout the academic year. Because of this, academic years 2024/25 and 2025/26 figures are partial. Data for academic years up to and including 2023/24 are complete.

Methodology

The model first estimates the number of borrowers expected at the end of academic years whose payment cycles are not finalised. It calculates the growth between the end of January and the end of the payment cycle in the most recent academic year with complete data. The model then increases the borrower numbers in the incomplete academic years by that growth. These figures are then appended to the historical timeseries and modelled.

The Doctoral and Masters forecasts are constructed separately using an ETS model (for details see Exponential smoothing (ETS) models section), set to heavily weight recent data when setting the level and the trend of the forecast, and apply a small degree of trend dampening. The intent behind the model settings is to inform the forecast with the growth observed in the years following the Covid-19 pandemic, which saw unusually high level of growth across the HE sector. In both forecasts, alpha and beta are set to 0.9 and 0.7, respectively. Phi is set to 0.95 in the Master’s forecast and 0.9 in the Doctoral forecast. These parameter values are relatively high, meaning the model places strong emphasis on recent observations, ensuring forecasts are responsive to recent shifts. The forecast assumes that 73% of Master’s entrants will study on a full-time basis and 27% on a part-time, and that 62% of Doctoral students will study full-time and 37% part-time.

A small number of EU nationals with pre-settled status are added to these forecasts. These groups are expected to stay flat until 2026/27 based the growth observed in their numbers in the last 3 academic years. From 2026/27 the pre-settled status will no longer exist and therefore no new borrowers with pre-settled status will take out SFE loans. As a result, this group drops out the forecast.

Forecast

Table 3.1 Forecast for the post-graduate entrant loan borrowers at HE providers in England and the devolved administrations

Academic Year

Masters entrant borrower forecast

Annual growth

Doctoral entrant borrower forecast

Annual growth

2025/26

62,100

6.6%

2,700

9.6%

2026/27

65,100

4.8%

2,900

6.4%

2027/28

68,300

4.9%

3,100

6.1%

2028/29

71,300

4.4%

3,200

5.2%

2029/30

74,200

4.0%

3,400

4.4%

2030/31

76,900

3.7%

3,500

3.8%

Assumptions

The forecasts assume that no changes will be made to loan eligibility policies over the forecast period.

Payment cycles (and therefore borrower numbers) are deemed complete one year after the end of the academic year a borrower started their course on, based on the progression of borrower numbers in previous payment cycles.

The model assumes that growth across the most recent complete payment cycle is a good enough proxy for growth across payment cycles that are not yet complete.

The model assumes recent years (2023/24–2025/26 as of April 2026) are more representative of future demand than earlier years.

The model assumes no capacity constraints in postgraduate provision over the forecast period.

Uncertainties

The growth in the forecast is informed by a relatively small number of academic years, which makes the forecast inherently uncertain.

Masters and Doctoral loans are relatively new compared to undergraduate loans, having only been introduced in 2016/17 and 2018/19, respectively. There is uncertainty on whether borrower behaviour has yet stabilised.

Data quality

The model uses SLC administrative data to determine entrant borrower numbers. The DfE receives data reports on postgraduate loans from the Student Loans Company quarterly basis. SLC publishes a statement on its administrative sources (opens in new tab).

The student loan outlay model forecasts loan amounts that the Department for Education (DfE) expects to pay higher education students (and their providers) via the Student Loans Company (SLC).

A range of sub-models are used to capture the various loan types available to students. The loan products that outlay forecasts are produced for are:

Full-time undergraduate loans (Plan 2) – the loan system for students on full-time courses that started between September 2012 and 31st July 2023 and that are eligible for undergraduate student support funding, consisting of fee loans and maintenance loans.

Part-time undergraduate loans (Plan 2) – the loan system for students on part-time courses that are eligible for undergraduate student support funding. These first became available in September 2012, consisting of a tuition fee loan. From August 2018, maintenance loans were also available to some part-time students.

Full-time undergraduate loans (Plan 5) – the loan system for students on full-time courses that start on or after 1st August 2023 and are eligible for undergraduate student support funding, consisting of fee loans and maintenance loans.

Part-time undergraduate loans (Plan 5) – the loan system for students on part-time courses that start on or after 1st August 2023 and are eligible for undergraduate student support funding, consisting of fee loans and maintenance loans for some part-time students.

Postgraduate Master’s loans (Plan 3) – loans available to Master’s students to help cover fees and living costs. They were introduced in August 2016 and are on the Plan 3 repayment system.

Postgraduate Doctoral loans (Plan 3) – loans available to Doctoral students from August 2018 to help cover fees and living costs. They are on the Plan 3 repayment system.

Outlay forecasts for Plan 1 loans are no longer produced due to the negligible number of recipients expected in the academic year 2025/26, because most students who started a course before September 2012 have now completed those studies.

Eligible English-domiciled students are entitled to tuition fee and maintenance loans for courses that are eligible for undergraduate funding, and Master’s and Doctoral loans for courses that are eligible for postgraduate funding. Previous publications included a separate ‘EU borrower’ forecast, for EU domiciled students who were eligible to take out tuition fees loans only. In the 2021/22 academic year this student finance support was withdrawn following the UK’s exit from the EU and the residency status that defines this small group of borrowers with partial eligibility has changed. Partial eligibility covers those who do not have access to undergraduate maintenance funding but have access to postgraduate funding and undergraduate tuition fee-only funding. This group now comprises a mixture of:

EU nationals with pre-settled status,

EU, other EEA and Swiss nationals still eligible for tuition fee loans as a result of the Withdrawal Agreement, including Irish nationals who have not been domiciled in the UK for 3 years before starting studies,

Other residencies granted partial higher education support under the regulations.

This group is now labelled ‘Borrowers granted partial higher education support under the regulations’. Both this group and English domiciled students are entitled to the same amount for postgraduate loans, but the two groups are forecast separately to capture the difference in their expected growth. For further details on loans and eligibility, please see the Student Finance England practitioner website (opens in new tab).

whether they have a Teaching Excellence and Student Outcomes Framework (TEF) rating, and

whether they have an Access and Participation Plan (APP) approved by the OfS.

For the 2025/26 academic year, approved (fee cap) providers with an approved APP can charge higher fees for full-time students:

up to £9,535 with a TEF award, and

up to £9,275 without a TEF award.

If an Approved (fee cap) provider does not have an approved APP, they can only charge the basic fee amount:

up to £6,355 with a TEF award, and

up to £6,185 without a TEF award.

Providers registered in the Approved category are not subject to fee limits. However, students at these institutions are only eligible for student support up to the basic fee cap that applies to Approved (fee cap) providers.

Maintenance loans for eligible students depend on their location and household income (where a borrower applies for a means tested loan). The maximum maintenance loan for full-time Plan 5 borrowers living away from home and studying outside of London, in academic year 2025/26 is £10,544, as outlined in the financial memorandum (opens in new tab). Table 1A of the Student Loans Company statistical publication Student support for higher education in England (opens in new tab) presents the maximum rates of maintenance loans and tuition fee loans for full-time students domiciled in England.

Maintenance loans became available in academic year 2018/19 to part-time, on-campus, degree students. These loans mirror the full-time maintenance loan, with the intensity of study considered alongside means testing and location. Students studying courses at less than 25% intensity are not eligible for part-time maintenance loans.

As part of a wider reform of the higher education system, the Government introduced the Lifelong Learning Entitlement (opens in new tab) Bill. Students will be able to apply for Lifelong Learning Entitlement funding from September 2026 and commence study from January 2027. This policy change is not included in the forecasts presented but will be integrated for future publications.

Postgraduate Master’s loans

The postgraduate Master’s loan was introduced in the 2016/17 academic year. Eligibility for a Master’s loan depends on the duration and intensity of the student’s course, their age on the first day of the first academic year of their course, and their nationality or residency status. The course must also be provided by a university or college in the UK, which is either publicly funded or a designated private provider. From the 2019/20 academic year, English providers are required to register with the OfS as Approved (fee cap) or Approved to be eligible for student support funding.

Unlike undergraduate loans, Master’s loan entitlement for eligible students depends on the start date of their course, rather than location or household income. The maximum Master’s loan amount for a course starting in the 2025/26 academic year is £12,858 across the length of the course.

Postgraduate Doctoral loans

The postgraduate Doctoral loan was introduced in the 2018/19 academic year. Eligibility for a Doctoral loan is based on the duration of the student’s course, their age on the first day of the first academic year of their course, and their nationality or residency status. The course must also be provided by a university or college in the UK, which is either publicly funded or a designated private provider. From the 2019/20 academic year, English providers are required to register with the OfS as Approved (fee cap) or Approved to be eligible for student support funding.

Doctoral loan entitlement for eligible students depends on the start date of their course. The maximum Doctoral loan amount for academic year 2025/26 is £30,301 across the length of the course.

Methodology

Student loan outlay, for undergraduate higher education loan products (including postgraduate Initial Teacher Training, which is funded through undergraduate student finance), is forecast based on historical data from the Student Loans Company. For postgraduate loan products, where historical information is limited, an alternative forecasting method is required.

Undergraduate higher education loan products

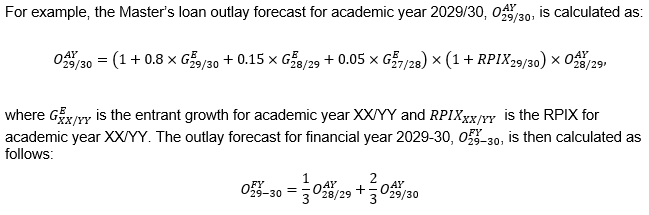

The student loan outlay forecasts for higher education Plan 2 and Plan 5 loan products use historical anonymised data on individual loan borrowers from the Student Loans Company. This data contains information on student loans and loan borrowers for academic years up to and including 2024/25 and has an effective date of 30th April 2025. Using this and other information from SLC and growth rates from the entrant borrowers model, forecast students are generated and allocated loans according to announced loan caps or historical loan amounts adjusted by OBR RPIX (Retail Price Index All Items Excl. Mortgage Interest) forecasts. Note that fee and maintenance loan levels available to students are typically already known for the first two or three academic years for which the model produces forecasts, currently 2025/26 and 2026/27 for maintenance loans, and 2025/26 up to and including 2027/28 for fee loans. Maximum fee amounts in the academic years 2025/26 up to and including 2027/28 are increased by 3.1% in 2025/26, and by 2.7% in 2026/27 and 2027/28. For the academic years 2025/26 and 2026/27 the maintenance loan entitlements were increased in line with the latest Office for Budget Responsibility (OBR) RPIX central forecast (opens in new tab) for the Jan-Mar quarter in each year.

This modelling method assumes that the distribution of characteristics of future loan borrowers, such as means-testing, sex and degree subject, is the same as for loan borrowers from the recent past. Internal analysis of historical trends in recent SLC data indicates that this assumption is generally accurate for most characteristics. Any policy changes to student finance brought in, such as the increase in tuition fees in the 2026/27 academic year, may impact on the distribution of the characteristics of loan borrowers and on their loan amounts. This is being monitored by DfE, and if needed, or where future policies are announced, an assessment will be made on the impact of the policy on the borrower numbers and loan amounts and the forecasts may be adjusted accordingly.

When the individual-level data was received from SLC with effective date April 2025, it contained nearly complete data for the 2024/25 academic year. To use this most recent year of data for modelling, estimates of the missing information until the end of the academic year, from April to August 2025, were made and the dataset amended accordingly. There are three main types of missing information between April and August, and these were quantified to produce a mini forecast of a full year of data for academic year 2024/25. These three types of information are:

Missing borrowers. By April, most loan borrowers in the academic year have been paid a loan amount by SLC. However, some students may not yet appear in the dataset because their first loan payment is later in the academic year, for example if their course starts between April and August, or if a student’s circumstances change and they require student finance when they did not earlier in the year. Borrowers can apply for funding up to 9 months after starting and later applications can also be honoured by SLC, so borrower numbers can change after the end of the academic year. The number of missing borrowers was calculated using SLC data on the total number of students at the end of August 2025, split by institution type, study mode, student domicile (England or ‘Borrowers granted partial higher education support under the regulations’), and loan product. To account for late reporting after the end of the academic year, the number of August borrowers was uplifted by the growth in the number of enrolled borrowers in academic year 2023/24 from the SLC August 2024 to the SLC April 2025 individual-level data, split by study mode, domicile, and for England-domiciled full-time students, by institution type too. For each combination of characteristics, this uplifted figure was compared to the number of students in the individual-level SLC April 2025 data, and a number of students equal to the difference in the April and uplifted August totals was added to the individual-level dataset. These records are created by randomly sampling from a pool of missing borrowers and assigning new unique identifiers. The missing borrower sample pool consists of individuals who are not present in the April 2025 extract but appear in the August 2025 extract. This approach captures both new entrants and returning borrowers who are introduced into the dataset later in the year.

Missing withdrawals. Some students will withdraw from university between April and August of an academic year, and this information will not have been contained in the April 2025 extract for the 2024/25 academic year. In addition, there is a (non-negligible) time lag between a student’s withdrawal and the HE provider notifying SLC of that event, so some information on withdrawals up to end April 2025 is missing too. To calculate the number of extra withdrawals in the 2024/25 academic year, the April 2025 extract was compared with the April 2024 extract, with the 2025 extract providing an updated view on withdrawals in 2023/24. Specifically, the proportion of missing withdrawals by study mode, institution type and loan product received was estimated. Within each of these combinations of characteristics, the expected number of extra withdrawals in 2024/25 was then randomly sampled and their records amended to add withdrawal information.

Missing loan outlay. Most loan outlay is paid prior to April in each academic year and is therefore recorded in the April cut of the SLC data. However, students who start later in the academic year, or whose circumstances change, may receive loan payments later than April and not all borrowers are paid their requested loan amount. The payments and requested loan amount for the 2023/24 academic year, i.e., the most recent full academic year of data in the 2025 extract, were compared across two years of April SLC data extracts (2024 and 2025). The proportion of borrowers with a requested loan amount in the April 2024 extract that had been paid less than that amount in the April 2025 extract was calculated, split by study mode, provider type and (requested) loan product. For each of these combinations of characteristics, the April 2025 SLC data was searched for students who had received less than their requested loan amounts and had not withdrawn in the 2024/25 academic year. A random sample of these students had their loan amounts increased to their requested amounts, based on the aforementioned proportions.

Once this missing academic year 2024/25 data had been imputed, the now-full year of data was used as the undergraduate outlay forecast baseline.

For borrowers who have not finished their course yet, their original course length is not always representative of the number of years of loans a borrower will go on to receive. For example, a borrower may repeat a year, switch courses to include or remove a placement year, transfer onto a new course entirely (starting in year 1 again) or withdraw. To reflect this in the outlay forecasts, once the full year of 2024/25 academic year data had been imputed, continuation rates reflecting average course lengths were applied to all students who were studying in the 2024/25 academic year and started their course after the 2018/19 academic year. These continuation rates were derived from the academic years 2014/15 and 2015/16 HESA student record data for full-time students, whereas for part-time students the continuation rates are based on the academic years 2016/17 and 2017/18 aggregate SLC data on part-time students taking up tuition fee loans. This adjustment was applied randomly within each study mode and for each original course length.

This data could now be used to generate students starting in future academic years. Entrant borrowers in the academic year 2024/25 were sampled, duplicated and renamed with new date information to generate entrants in future years. Generated entrants were all assigned Plan 5 repayment terms. The number of students to be generated for each future year was calculated by applying the student entrants forecast growth rates to the number of 2023/24 entrants from aggregate SLC data. Different growth rates are calculated for part and full-time students and England and tuition fee loan-only eligible students, so the new students were generated for each combination of these characteristics. Some subsections of the student population were separated out and generated using a set entrants forecast, for example where a student numbers cap was in place. These sets of students included Nursing, Midwifery and Allied Health (NMAH) students, students studying Medicine and Dentistry, postgraduate Initial Teacher Training students, students studying at alternative providers, and Higher Technical Qualification (HTQ) students. Students in these groups were identified by a combination of CAH (Common Aggregation Hierarchy) 01 code, qualification level, course duration and course level.

Some students may be eligible to receive funding for more than one HE Plan 2 or Plan 5 course; examples include postgraduate teacher training students, students completing a foundation degree before continuing to study for a bachelor’s-level degree, or students studying an Equivalent or Lower Qualification (ELQ)-exempt course. Students studying more than one funded course therefore usually already have a loan balance when they start their second course. The entrants generated by the method above did not have pre-existing loan balances. To generate a realistic loan borrower population where some entrants each year already have a loan from a previous course, a stratified sample (by study mode and domicile) of previous loan borrowers was chosen. These borrowers were allocated to start new courses, with the proportion starting at different institution types, course levels and subjects (Medicine and Dentistry, Initial Teacher Training, and all other courses) determined by analysis of historical SLC data. These borrowers with previous loans made up a small portion of the forecast entrant numbers.

At this point in the modelling process, the SLC data consisted of a row per student per course with their loan outlay recorded up to the end of 2024/25 (some of which is estimated). It also included future students generated from current and previous students and renamed with their date information shifted forwards. With this data, future outlay can be generated.

To generate future outlay, the outlay of each student was calculated as the lower of their most recent year of outlay 2024/25, or their course start year if later) uprated by the OBR forecast of RPIX, and the relevant loan cap. For full-time students that started prior to 2024/25 and were identified to be on a year overseas or a placement year in 2024/25, their future outlay was based on their outlay in 2023/24 instead. Separate tuition fee caps were applied to students at Approved and Approved (fee cap) providers, set to the maximum tuition fees for each type of institution. Maintenance loan caps were applied separately to medical and dentistry students in their fifth and sixth years (who are eligible for smaller loans because they receive an NHS bursary in these years), and to all other students. Additionally, a random sample of students on courses of length 4 years were chosen to be sandwich placement students and were given lower fee and maintenance loans in their third years, where their third year was 2025/26 or later. A random sample of entrants starting in 2024/25 who had fee loans below the cap in that year were chosen to be studying courses as fee waiver students, and allocated fee loans at the cap in their second year, even where this was an above-inflation increase. A random sample of part-time HTQ borrowers were allocated an HTQ-specific maintenance loan calculated based on SLC data on existing borrowers taking level 4 & 5 qualifications. The proportions of students who have sandwich placement, fee waiver, nursing bursary loan or HTQ maintenance loan adjustments were determined either by an analysis of SLC data or provided by the OBR.

The academic year loan outlay forecasts were converted into financial years. This was done based on an analysis of academic year payments and which financial year they fall in, using SLC data. This analysis took into account at which point within an academic year a student started. Payments relating to one academic year can span multiple financial years. Those students starting later in an academic year will have larger portions of their loan paid in the later relevant financial years. At this point, forecasts of total loan outlay as well as a breakdown by Plan type were produced.

Master’s loans

Master’s loans were introduced in academic year 2016/17. The Master’s loan outlay forecast is informed by the number of entrant borrowers forecast by the Postgraduate entrant borrower model in each academic year and aggregate‑level historical postgraduate loan data from the Student Loans Company (SLC). As Master’s loans are entitlement‑based for the whole course rather than paid annually, the approach to forecasting differs from that used for undergraduate loans.

Table 4.1: Core Master’s loans model parameters by course duration

Course duration

Proportion of loan recipient entrants

2016/17 average loan (per year)

1 year

0.80

£9,300

2 years

0.17

£4,400

3 years

0.03

£2,700

Loan outlay for each academic year is calculated using a cohort approach, based on start year and the proportion of students within each course duration. The parameters used are shown in Table 4.1, where average loan amounts are rounded to the nearest £100. The average loan amounts per year are derived from 2016/17 academic year SLC payments data. The proportions of loan recipient entrants are based on a combination of 2017/18 academic year SLC data and comparisons between the 2018-19 financial year model forecast to outturn. The expected number of loan borrowers in each cohort is multiplied by an estimated average loan amount. The estimated average loan amounts per year for a cohort are calculated by uprating the 2016/17 academic year average loan amounts by OBR outturn and forecast RPIX, from the 2017/18 academic year to the corresponding start year. The loan amount is spread across one, two or three years depending on course duration. The sum of the outlay from each cohort is aggregated to produce a final academic year outlay figure. The financial year forecast is calculated by assuming the outlay in a given financial year is equal to the sum of one third of the outlay in the first academic year it overlaps with and two thirds of the outlay in the second academic year it overlaps with.

Doctoral loans

Doctoral courses can last from 3 to 8 years. The forecast assumes the same distribution of course duration in each year of the forecast, shown below in Table 4.2. This assumption is based the distribution of course lengths in Doctoral loan application data for academic year 2018/19, with an effective date of 15th November 2018.

Table 4.2:Estimated proportion of Doctoral loan recipient entrants by course duration

Course duration

Proportion of loan recipient entrants

3 years

0.43

4 years

0.33

5 years

0.06

6 years

0.10

7/8 years

0.07

Figures may not appear to sum to 1 due to rounding.

The average loan for the whole course is estimated using a similar uprating approach to the Master’s forecast. For example, the average loan for new entrants in the 2025/26 academic year is estimated to be £ 28,968 for their whole course. This is calculated by uprating the average requested amount in 2018/19 (opens in new tab) as at end December 2018, by outturn and forecast RPIX, from the 2019/20 academic year to the corresponding start year. Note, the maximum doctoral loan amount for a course starting in 2025/26 is £ 30,301.

Annual academic year outlay is then calculated using a cohort approach based on course duration. The number of borrowers per course duration as outlined above, is multiplied by continuation rates from HESA data, to estimate the expected number of borrowers in each year for each course length. The expected number of loan borrowers in each cohort is multiplied by the corresponding average loan amount spread evenly across the course duration. The sum of the outlay from each cohort is aggregated to produce a final academic year outlay figure. Like in the Master’s loans forecast, the financial year forecast is calculated by assuming the outlay in a given financial year is equal to the sum of one third of the outlay in the first academic year it overlaps with and two thirds of the outlay in the second academic year it overlaps with.

Long-term outlay forecasts

The same methodology as documented above was used to forecast the long-term full-time and part-time undergraduate outlay, however, an alternative method was used to forecast the long-term postgraduate outlay.

Undergraduate higher education loan products

The methodology described above, used to forecast outlay for undergraduate loans was also used to produce the long-term undergraduate outlay forecast. Using individual-level data on loan borrowers provided by SLC and long-term growth rates from the entrant borrowers model, forecast students were generated for each academic year from 2025/26 to 2083/84. These students were allocated loans using forecast loan caps based on announced loan caps and the long-term OBR RPIX forecast. The loan outlay forecast was converted to a financial year forecast by apportioning loan payments made in each academic year between the financial years they straddle, according to analysis of SLC data.

Postgraduate loans

The postgraduate long-term forecast is calculated using a cohort (based on start year) approach. The growth rate for each cohort is found by taking the entrant growth from the long-term student numbers model for the academic year that the cohort started. This is then multiplied by the proportion of total borrowers from each cohort, by product, shown in Table 4.3, to give a total student loan borrower growth rate for the academic year. This student loan borrower growth rate is then multiplied by the previous academic year outlay forecast and multiplied by forecast RPIX. The financial year forecast is calculated by assuming the outlay in a given financial year is equal to the sum of one third of the outlay in the first academic year it overlaps with and two thirds of the outlay in the second academic year it overlaps with.

Table 4.3: Proportion of total borrowers by postgraduate loan product and year of study

Year of study

Proportion of total borrowers (Master’s)

Proportion of total borrowers (Doctoral)

1st year

0.80

0.40

2nd year

0.15

0.30

3rd year

0.05

0.25

4th year

−

0.05

Data quality

Student loan outlay forecasts are uncertain as they are primarily driven by borrower behaviour as well as economic factors such as inflation and household residual income. This model assumes that the characteristics and behaviour of future borrowers will be similar to historical ones derived from SLC administrative data which may not necessarily be the case. The model is also dependent on the Spring 2026 OBR macroeconomic forecasts that are used to uprate loans. Any significant changes to the economy from these forecasts could affect the outlays that will be made on student loans.

The model uses SLC administrative data to determine borrower numbers and loan amounts. The DfE receives data extracts from the Student Loans Company on an academic year basis that are used in the student loan outlay model. This data is consistent with the data published in the SLC Student Support for higher education in England publication (opens in new tab). Data on borrower sex is collected at the application stage, the only options are ‘female’ or ‘male’, and options are self-identified by loan applicants.

The model uses the growth in forecast entrants from the DfE entrant borrowers model; see Section ‘Entrant borrowers model’. The population covered includes borrowers entitled to full support that will take out either a tuition fee or a maintenance loan from Student Finance England studying at Approved (fee cap) providers but does not cover borrowers at Approved providers.

The model assumes that loans will be uprated by forecast RPIX in future years for which the maximum loan amounts have not yet been announced. With the exception of the introduction of the LLE, the model incorporates existing government policy announced by 24 April 2025 and assumes such policy will remain unchanged. Therefore, the introduction of the LLE and, if implemented by Government, any other changes to student loan eligibility, terms and conditions could affect the forecasts presented in this publication.

Table 4.4 compares the performance of the loan outlay model to SLC outturn data in 2025-26 and shows that the overall outlay forecast was approximately 1.9% lower than the outturn figure relative to the forecast. This equates to £405 million. The Undergraduate forecast was lower than the outturn with a percentage difference of -1.8% relative to the forecast. The Master’s and Doctoral forecasts were lower than the outturn with percentage differences of -3.3% and -18.7% relative to the forecast respectively.

Table 4.4: Difference between Higher Education Outlay Forecast and SLC outturn for financial year 2025-26

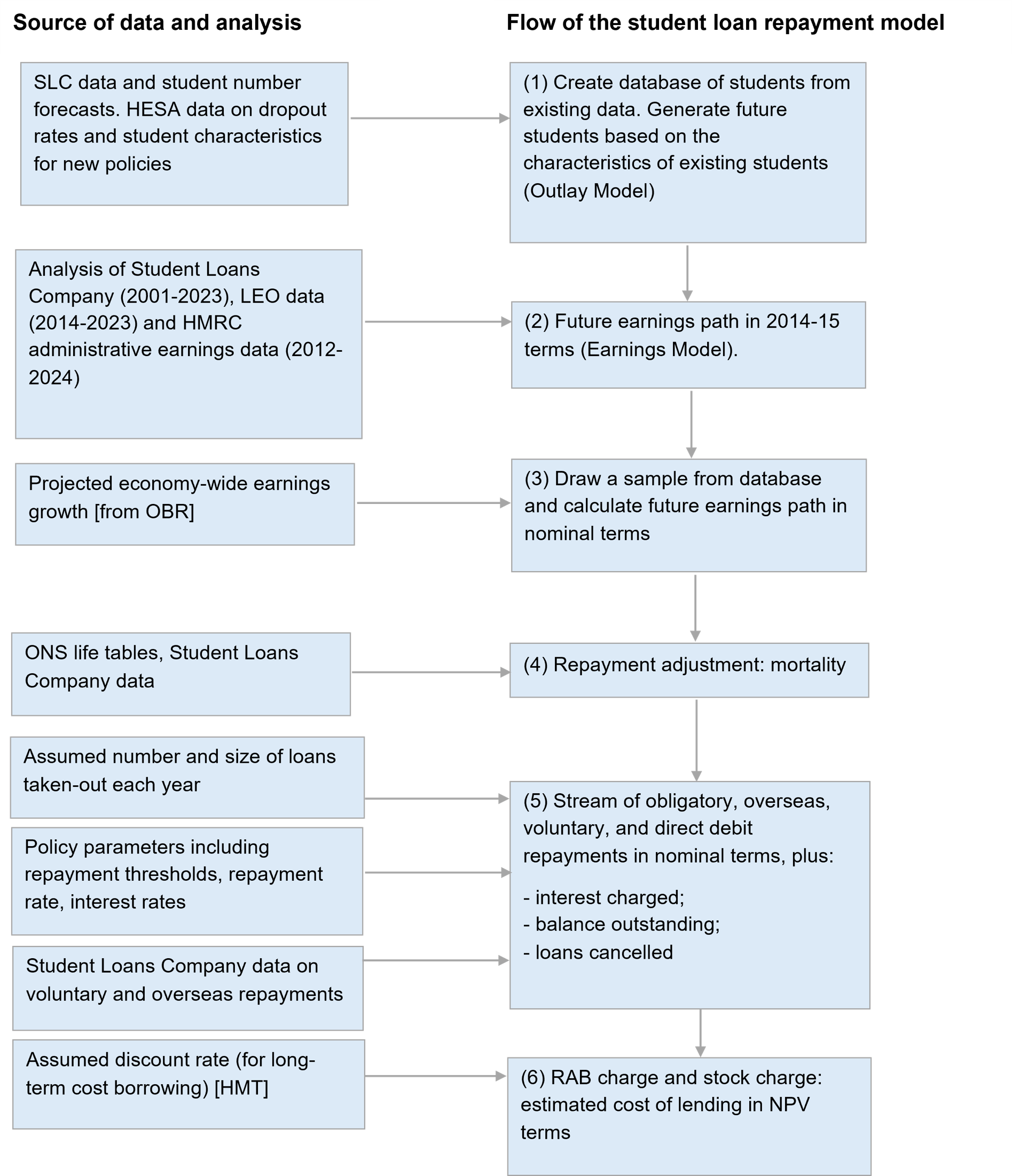

The DfE student loan earnings and repayments model is the financial model used to estimate the cost of income-contingent student loans to Government. It forecasts the repayments that the Department expects to receive on its expenditure on student loans.

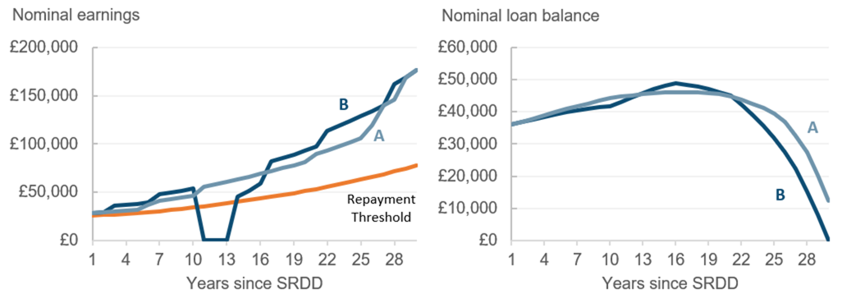

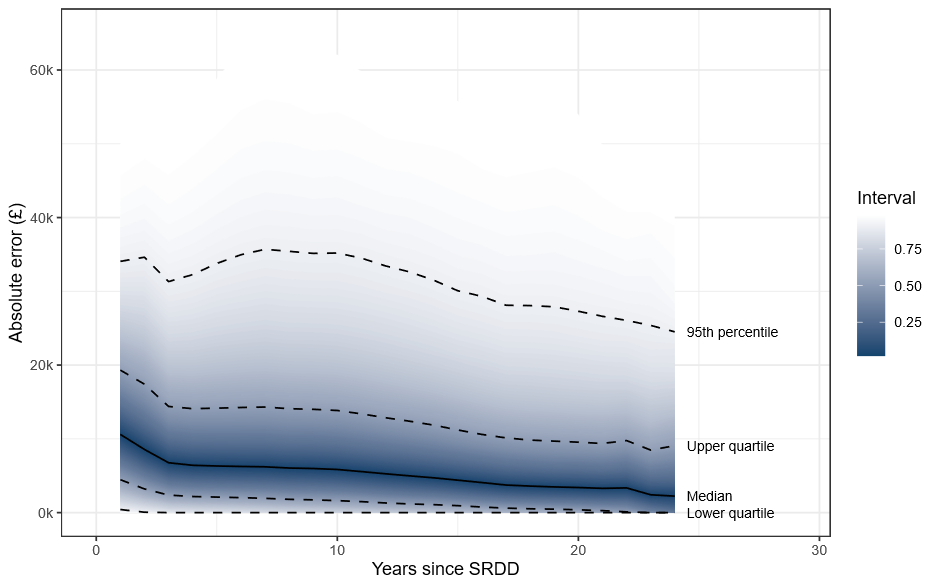

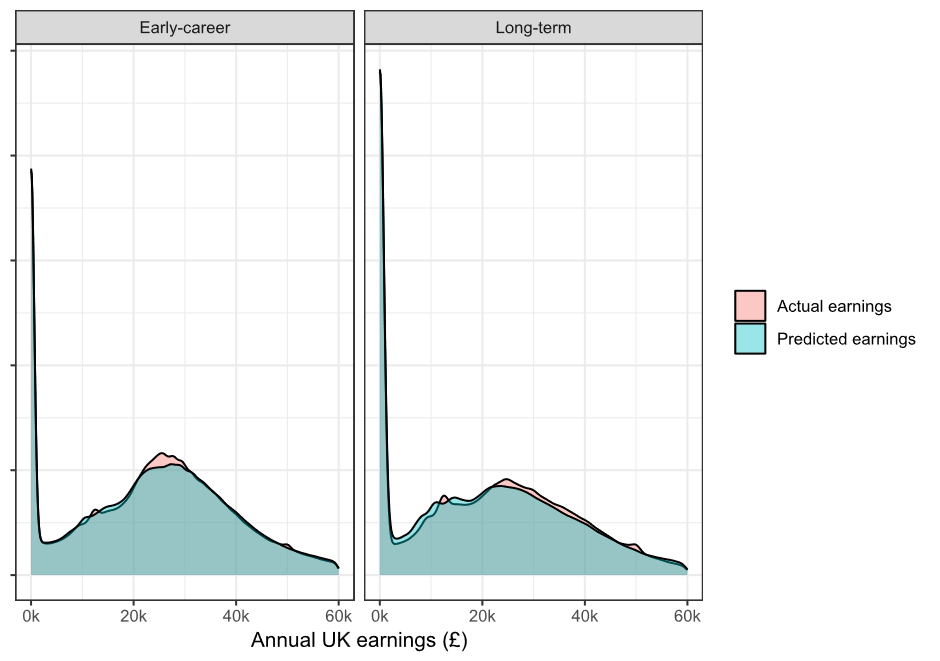

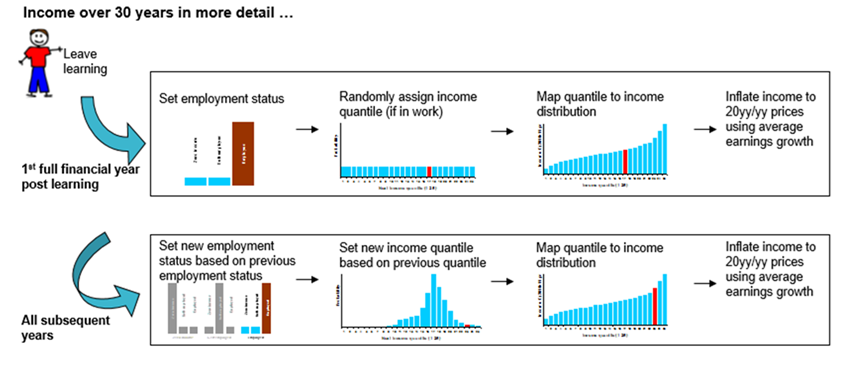

The model is a micro-simulation model. It forecasts student loan repayments by estimating future earnings for a sample of individual student loan borrowers, and applies the loan repayment policy to each borrower, before aggregating the results to estimate totals for the population as a whole. For each loan borrower, it predicts their next year’s earnings, and when this is repeated it generates an earnings path. Where historical information on earnings is available the model makes use of this. Earnings predictions are based on the borrower’s level of study, sex, years since SRDD (Statutory Repayment Due Date, typically the April following the borrower’s final point of outlay), age and other information. This allows the model to capture individual changes in earnings over the borrower’s working lifetime.

Once a borrower’s earnings have been forecast, their repayments, interest and loan balances are calculated year by year for the length of their repayment term, or until they finish repaying their loan. Further adjustments are made to some borrowers’ repayments to allow for voluntary repayments, overseas repayments, and differing obligatory repayments resulting from non-standard earnings distributions across months of the year or across multiple jobs (frictions).

The model forecasts repayments for income-contingent student loans eligible through Student Finance England. Earnings forecasts are made for undergraduates (first degrees and sub-degrees) and PGCE loan borrowers based on historical administrative data for comparable loan borrowers and historical administrative earnings data for the UK residents. For Master’s and Doctoral loan borrowers, earnings are modelled by applying a percentage uplift to an earnings forecast for a comparable first degree student.

The main data sources used in the model are:

Student Loans Company (SLC) administrative data – provides details of borrowers and the loans they take out, used to forecast earnings and employment status in early repayment years. Used for modelling migration, repayment frictions and repayments made directly to the SLC.

Longitudinal Education Outcomes (LEO) - used in earnings and employment models in early repayment years.

His Majesty’s Revenue and Customs (HMRC) administrative earnings data – used in earnings model from year 11 of repayments onwards.

Office for National Statistics (ONS) life tables – data on deaths.

ONS Average Weekly Earnings (AWE) data – used to adjust earnings between 2014-15 earnings values and nominal terms.

Student Loans Company (SLC) administrative data – used to estimate course completion rates and borrower characteristics for postgraduates, replacing HESA data which was used prior to April 2026.

Office for Budget Responsibility (OBR) macroeconomic forecasts – forecasts of earnings growth, the Bank of England base rate, RPI and RPIX published as part of their Economic and Fiscal Outlook EFOs - Office for Budget Responsibility (opens in new tab).

DfE Student numbers model – forecasts of entrant numbers.

DfE Outlay model – forecasts of student loan outlay.

Figure 5.1: Processes and sources underlying the student loan repayment model

Figure 5.1 explains, at a high level, the processes that the model goes through to produce the forecasts, along with how each data source feeds into the full model.

Student loan repayment policies

Income Contingent Repayment (ICR) loans require borrowers to make repayments based on their annual income, starting from the April after they have left their course (the borrower’s SRDD). Under each repayment plan, borrowers are required to make repayments each tax year, through either PAYE or self-assessment, equal to a percentage of their income above a set repayment threshold until either they have fully repaid their loan balance, or their loan is cancelled. Loans are cancelled if the borrower dies, if they still have an outstanding loan balance at the end of their repayment term, or if they are in receipt of a disability related benefit and are assessed as permanently unfit for work. Loans accrue interest during and after the borrower’s course, which is added to their loan balance.

A borrower becomes liable to repay their loan on the 6th of April (start of the UK tax year) after they complete or withdraw from their course, at which point their repayment term starts on what is known as their Statutory Repayment Due Date (SRDD). There are two exceptions to this:

Part-time loan borrowers will enter repayment at the start of the tax year after four years have elapsed since the first day of the first academic year of the course, even if they are still studying.

When a loan product is first introduced, the earliest SRDD for some borrowers may be later than it would usually be. For example, all Plan 2 borrowers that completed or left their courses before April 2016 had an SRDD of April 2016, even though under the usual rule some would have had an SRDD up to three years earlier. For Plan 5 borrowers, the first possible SRDD is April 2026.

A summary of the key repayment policy details for each loan product is shown in Table 5.1 below.

Table 5.1: Key policy details for each loan product

Plan 1

Plan 2

Plan 3 (Postgraduate)

Plan 5

Earliest year of entrants

1998/99

2012/13

2016/17 (Master’s)

2018/19 (Doctorate)

2023/24

Earliest SRDD cohort

April 2000

April 2016

April 2019 (Master’s)

April 2020 (Doctorate)

April 2026

Length of repayment term

Until age 65 (entrants up to 2005/06);

25 years after SRDD (2006/07 entrants onwards)

30 years after SRDD

30 years after SRDD

40 years after SRDD

Repayment rate

9% of earnings above repayment threshold

9% of earnings above repayment threshold

6% of earnings above repayment threshold (in addition to any Plan 1, 2 or 5 repayments)

9% of earnings above repayment threshold

Interest rate

The lower of either RPI, or the Bank of England base rate +1%

RPI+3% during course, variable between RPI and RPI+3% after SRDD depending on earnings

RPI+3%

RPI

The interest rate applied to student loans is based on the Retail Price Index (RPI). The Department for Education (DfE) uses the RPI figure from the March prior to the start of the academic year to set interest rates for the following year. This ensures that the interest reflects inflation and maintains the real value of the loan over time. RPI will align with CPIH (Consumer Price Index including owner occupiers' housing costs) from 2030.

The interest rates for Plan 2, 3 and 5 student loans are subject to a Prevailing Market Rate (PMR) cap. This means borrowers will not be charged an interest rate greater than the reasonable market rate for an unsecured personal loan, with regular reviews of the cap published at Change to the Plan 2, Plan 5 and Plan 3 ('Postgraduate (PG)') student loan interest rates announcement - GOV.UK (opens in new tab). The PMR cap is currently, and is consistently forecasted as, higher than the maximum uncapped interest rate, so doesn’t currently have an effect on forecasts.

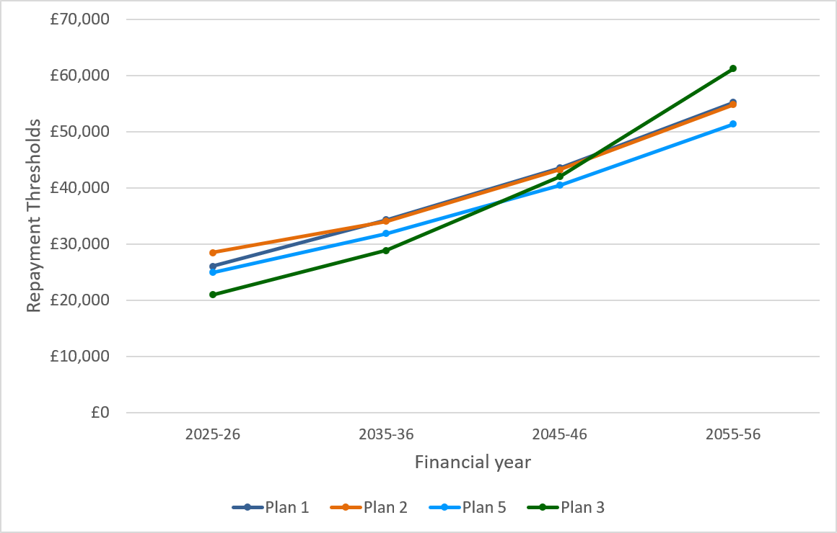

Each loan product has a separate income repayment threshold, above which repayments are made. Figure 5.2 shows the forecast repayment thresholds for each policy. All historical Plan 1, Plan 2 and Plan 3 threshold levels are published (opens in new tab), alongside Plan 4 thresholds which are applicable only to borrowers domiciled in Scotland.

The Plan 1 threshold is set at £26,065 for tax year 2025-26, and at £26,900 for tax year 2026-27. It will subsequently increase each year based on RPI.

The Plan 2 threshold was initially set at £21,000 from 2016-17 to 2017-18 before rising to £25,000 in 2018-19, to £26,575 in 2020-21, and to £27,295 in 2021-22. The threshold remained at £27,295 until the end of tax year 2024-25, after which it increased to £28,470 in line with RPI. The threshold will increase in line with RPI to £29,385 for tax year 2026-27 and will remain at this level until the end of tax year 2029-30. This is following the announcement at the 2025 Autumn budget to freeze the Plan 2 repayment threshold for 3 years from 2026-27. The Plan 3 repayment threshold is currently £21,000.

The initial Plan 5 repayment threshold is set at £25,000 until April 2027, at which point it will increase in line with RPI.

If a borrower has loans under multiple undergraduate plan types, they repay in line with the rules outlined at Repaying your student loan: How much you repay - GOV.UK (www.gov.uk) (opens in new tab). For example, if a borrower holds both a Plan 1 and a Plan 2 loan, they pay back 9% of income over the Plan 1 threshold. If their income is under the Plan 2 threshold, repayments only go towards the Plan 1 loan. If income is over the Plan 2 threshold, repayments will be split between both loans, with repayments on income between the thresholds going to the Plan 1 balance and income above the Plan 2 threshold going towards the Plan 2 balance.

Rules for borrowers with Plan 1/2 and Plan 5 loans are analogous to those with both Plan 1 and 2 loans.

Thestudent loan undergraduate repayment model forecasts future repayment thresholds for all undergraduate plan types using OBR forecasts for RPI, in line with legislation (opens in new tab).

Borrowers with a Plan 3 (postgraduate) loan repay this in parallel with any undergraduate loans (i.e. Plan 1, Plan 2 or Plan 5). Plan 3 repayments are calculated separately at 6% of income over the postgraduate threshold (£21,000 as of 2026) and are made in addition to the 9% repayment on income over the relevant undergraduate threshold(s). This means a borrower with both Plan 2 and Plan 3 loans could repay a total of 15% of their income above the respective thresholds.